For our Standard Fix & Flip, New Construction, and Bridge financing solutions, we typically provide terms that span from 12 to 18 months, with the specific term length tailored to the project’s size.

In the case of our DSCR rental loans, these come with a 30-year term, offering a range of options for prepayment penalties and adjustable-rate mortgages (ARMs). These ARMs can include interest-only periods, should the borrower choose.

For Micro Loans, Gator Loan, Gap Funding, or any other innovative financing approach, we typically aim for a high return with a maximum term of six months.

Bridge Loans

Bridge loans are short-term financing options used to “bridge” the gap between immediate financing needs and longer-term solutions. They are often used for fix-and-flip projects, construction of new homes, and acquisitions of multi-family or mixed-use properties. The documentation required typically includes:

Loan Application: A formal application providing the lender with details about the borrower and the project.

Photo ID: Identification to verify the borrower’s identity.

Title Agent/Attorney: Contact information for the professional handling the property’s title work and closing.

Borrower Experience: Documentation of the borrower’s experience in investing in properties, demonstrating capability and risk mitigation.

Purchase Contract: A contract showing the property is being purchased under the name of the entity borrowing the funds, ensuring legal and financial clarity.

Rehab List/Budget: Detailed plans and budgets for renovations and improvements on the property, providing a clear use of funds.

Operating Agreement, EIN Letter, and Articles of Organization: Documentation proving the legal existence and structure of the borrowing entity, along with its tax identification number.

Rental Loans

Rental loans are designed for investors looking to hold properties long-term to generate rental income. This includes traditional rentals, DSCR (Debt Service Coverage Ratio) loans, AirBnB rentals, the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat), multi-family, and mixed-use rentals. The requirements often encompass:

Loan Application: Similar to bridge loans, providing details on the borrower and investment.

Title Agent/Attorney: Ensuring there is a point of contact for title and closing matters.

Borrower Experience: A history of the borrower’s real estate investment activities, including purchasing, selling, and renting properties.

Purchase Contract: Required if the property is being purchased, under the name of the borrowing entity.

Lease Agreement: For rental properties, showing the property is generating or will generate income.

Photo ID: For identity verification.

Operating Agreement, EIN Letter, and Articles of Organization: Establishing the borrowing entity’s legal structure and tax status.

Payoff and 6 Month Payment History for Existing Lien: If refinancing, documentation of the current mortgage and payment history is required.

These documents collectively provide lenders with a comprehensive view of the loan’s purpose, the property involved, the borrower’s ability to manage and repay the loan, and the legal and financial structure of the borrowing entity. Proper preparation and understanding of these requirements can facilitate a smoother lending process for real estate investors.

Our lender’s legal fee ranges between $995 and $2000, and the processing fee ranges from $1525 to $2500. Additionally, there is a draw inspection fee of $300 for every draw request.

It’s important to note that we have flexibility with our points and fee structure. This means we have the capability to forego charging points and instead, generate our revenue through various fees.

Our loan interest rates vary depending on the loan type and duration, and are affected by the borrower’s experience, credit score, and the details of the transaction. Currently, the starting rates for our Fix/Flip, New Construction, and Bridge loans are at 9.75%. For our Rental DSCR loans, the starting interest rate is 6.87%.

Our minimum for rental DSCR loans is 680 for novice investors and 650 for seasoned investors.

If you require extra time and your loan is current, including up-to-date payments and insurance, we are willing to collaborate with you. We evaluate extension requests on an individual basis, offering options for 30 days, 3 months, and 6 months, depending on the specific circumstances. Please note, loan extensions are subject to an extension fee ranging from 1 to 2 points.

Our Fix and Flip, New Construction, and Bridge loans come without any prepayment penalties, allowing for flexibility in early repayment. However, our Rental DSCR loans include optional prepayment penalties with durations ranging from 1 to 5 years, providing various choices to suit different financial strategies.

Both the agreement and the borrower(s) are under consideration. The operator is one of the deal’s assets, and a bad borrower can ruin a good deal. We want to know if this is a good deal and whether we can be confident that the borrower will fulfill their end of the bargain by finishing the project on schedule and giving the money back.

Our loans are referred to as “light doc” loans since we only consider the deal specifics, borrower experience, creditworthiness, and liquidity. We do not look at tax returns or income verification; instead, we require evidence of liquidity in the form of bank statements and a stated income personal financial statement.

Regarding the loans that we originate, we have complete control over all loan decisions. As available, we allocate our own funds to specific projects and oversee various capital sources to offer our borrowers optimal choices and adaptability.

For a standard loan, we do not offer initial funding for construction. The reimbursement amount for completed work will be influenced by your arrangement with your contractors. You may request draw reimbursements upon completion of work and subsequent inspection. However, as a PERK, we are able to provide a portion of the construction budget upfront at the closing table to assist in kickstarting your project.

Commercial properties are permitted under our terms and bridge loans, but only multifamily and mixed-use properties with five or more units that are over $250,000 and comprise more than 50% residential space will be accepted. We don’t make loans for properties with special uses or for pure commerce.

After we finish the borrower interview, you can order both an insurance broker and a title company on your own if you have a preferred relationship with either. We can put you in touch with some of our recommended, carefully screened partners in each category if you would like recommendations on either. Each vendor’s contact information would be sent to us, and our staff would include it on all correspondence.

Indeed. We will carefully source the money prior to closing in order to close on the property and complete the project without running out of money. Before closing, the money would have to be transferred into a personal or business bank account. There is a three-month seasoning period for our Rental DSCR before all funds are released into your accounts.

Although lending on or refinancing with trust can be challenging, we can examine the trust documents case-by-case to identify any obstacles or whether lending to one would be prohibited. If we were able to lend to one, the trust would have to be irrevocable in every situation.

For our Fix & Flip, New Construction, and Bridge loans, the closing period is usually set between 2 and 3 weeks. On the other hand, our Rental DSCR loans tend to close within a 4 to 5-week timeframe. That said, we can hasten this process if provided with exceptional levels of responsiveness, organization, and readiness. Moreover, our Fast-Track Process offers a way to significantly shorten this duration.

Opting for Fast Track allows you to receive priority processing for title, appraisal, and insurance services at the point of loan application, substantially cutting down on the processing time.

A member of our team will get in touch with us once our application has been finished and submitted to discuss the deal and the details—financials, experience, and next steps, among other things. If we decide to proceed after the borrower interview call, we will order the appraisal from one of our pre-screened sources through an approved appraiser or an Appraisal Management Company.

Levine Capital offers Earnest Money Deposit (EMD) funding in most U.S. states, with the exception of California (CA), Hawaii (HI), Utah (UT), Vermont (VT), and Kansas (KS), per our current eligibility guidelines.

We use cookies to improve your experience on our site. By using our site, you consent to cookies.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Google Tag Manager simplifies the management of marketing tags on your website without code changes.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Facebook Pixel is a web analytics service that tracks and reports website traffic.

Service URL: www.facebook.com (opens in a new window)

A video-sharing platform for users to upload, view, and share videos across various genres and topics.

Service URL: www.youtube.com (opens in a new window)

Levine Capital's Ground Up Construction Loans give real estate investors the leverage and flexibility to break ground faster. Competitive terms, investor-first underwriting, and capital structured around your 1-4 unit residential build.

Private capital built around how serious real estate investors actually operate.

Two purpose-built programs designed around your track record and project scope.

Bringing a modular build to market? We finance modular home projects nationwide under our Ground-Up Construction program.

Nationwide coverage across our active lending markets.

Get a fast, no-obligation quote from a lender that closes when it counts.

* Non-owner-occupied loans only. All products are intended for residential investment properties.

** Rates shown reflect the lowest available pricing. Actual rates and terms are subject to approval criteria including FICO, experience, ownership duration, and other underwriting factors.

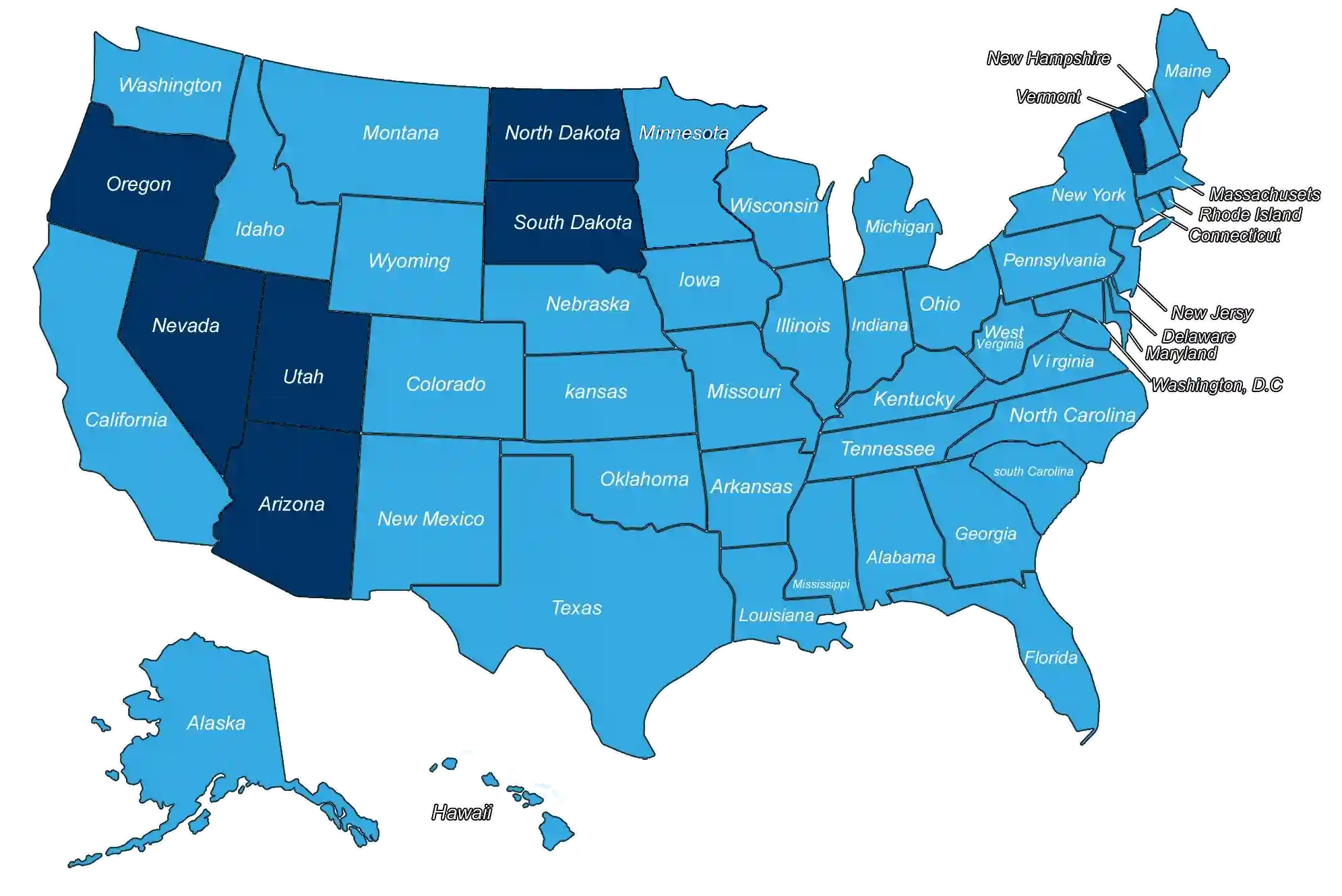

*** Levine Capital does not currently lend in: Arizona, Nevada, North Dakota, Oregon, South Dakota, Utah, and Vermont.