Here’s the fine print for what we’re looking for as an accredited investor:

An investment involves a degree of risk and is appropriate only for persons having suitable financial resources who understand the long-term nature of, and risk factors associated with such investment.

Participation in any of Levine Capital Management, LLC (“LCM”)’s investments is being offered in reliance on the exemption from registration under the Securities Act of 1933, as amended (the “Act”) as a transaction not involving any public offering provided by Section 4(2) of the Act and Regulation D promulgated hereunder (“Regulation D”). As a consequence, participants will be prohibited from reselling their participation unless the Securities are subsequently registered or an exemption from such registration is available under the applicable federal and state laws.

As a result of the lack of marketability of the investment and the risks associated with such investment, participation is suitable only for investors who have other adequate financial resources. Accordingly, subscriptions will be accepted only from prospective investors for whom LCM, in its sole discretion, determines the investment to be suitable.

LCM will accept participation, only from Accredited Investors. An investor will be deemed an Accredited Investor only if he or it, as the case may be, meets one of the following tests: (1) he is a natural person who has, at the time of his participation, a net worth or joint net worth with his spouse exceeding $1,000,000; (2) he is a natural person who had an individual income in excess of $200,000 or joint income with his spouse in excess of $300,000 in each of the two most recent years and has a reasonable expectation of reaching the same income level in the current year; (3) it is either (a) a bank as defined in Section 3(a)(2) of the Act or any saving and investment association or other institution as defined in Section 3(a)(5)(A) of the Act whether acting in its individual or fiduciary capacity, (b) a broker or dealer registered pursuant to Section 15 of the Securities Exchange Act of 1934, (c) an insurance company as defined in Section 2(13) of the Act, (d) an investment company registered under the Investment Company Act of 1940 or a business development company as defined in Section 2(a)(48) of such Act, (e) a Small Business Investment Company licensed by the United States Small Business Administration under Section 301(c) or (d) of the Small Business Investment act of 1958 or (f) an employee benefit plan within the meaning of Title I of the Employee Income Retirement Income Security Act of 1974, if the investment decision is made by a plan fiduciary as defined in Section 3(21) of such Act, which plan fiduciary is either a bank, saving and loan association, insurance company or registered investment advisor or if the employee benefit plan has total assets in excess of $5,000,000 or if a self-directed plan, with investment decisions made solely by persons that are Accredited investors; (4) it is a private business development company as defined in Section 202(a)(22) of the Investment Advisors Act of 1940; or (5) an organization described in Section 501(c)(3) of the Internal Revenue Code of 1986 (the “Code”), corporation, Massachusetts or similar business trust or partnership not formed for the specific purpose of participation with total assets in excess of $5,000,000; (6) a trust, with total assets in excess of $5,000,000 not formed for the specific purpose of participating in the Investment, whose participation is directed by a person who has such knowledge and experience in financial and business matters that he is capable of evaluating the merits and risks of an investment in investment participation; or (7) it is a corporation, partnership, trust or other entity and each and every equity owner of such entity certifies that he meets the qualifications set forth in either (1), (2), (3), (4), (5) or (6) above.

In addition, an individual investor, or each equity owner of an entity described in clause (7) of the proceeding paragraph, must either (i) have a net worth of $1,000,000 at the time of his participation and an individual income in excess of $200,000 in each of the most recent two years and a reasonable expectation of reaching the same income level in the current year or (ii) have a net worth of $2,000,000 at the time of his participation and an individual income in excess of $100,000 in each of the most recent two years and a reasonable expectation of reaching the same income level in the current year.

The term “net worth” means the excess of total assets at fair market value, excluding home and home furnishings, over total liabilities excluding home mortgages, but including estimated income taxes payable on unrealized appreciation of assets. In determining income, “individual income” and “joint income” mean adjusted gross income as reported for federal income tax purposes (less any income attributable to a spouse, or to property owned by a spouse in the case of “individual income”) increased by the following amounts (but not including any amounts attributable to a spouse or to property owned by a spouse in the case of “individual income”): (i) the amount of any interest income received which is tax exempt under Section 103 of the Code; (ii) the amount of losses claimed as a limited partner in a limited partnership (as reported on Schedule E of Form 1040); (iii) any deduction claimed for depletion under Section 611 et seq. of the Code; and (iv) any amount by which income from long-term capital gains has been reduced in arriving at adjusted gross income pursuant to the provisions of Section 1202 of the Code.

In addition, participation will be permitted only to persons who represent, among other things (i) that they are participating in the Investment for their own accounts, for investment only and not with a view toward the resale or distribution thereof, (ii) that they have such knowledge and experience in financial and business matters that they are capable, either alone or together with one or more advisors, of evaluating the merits and risks of participating in such Investment(s), (iii) that they and their advisors have been provided the opportunity to ask questions and receive answers concerning the terms and conditions of such participation and to obtain any additional information which LCM possesses or can acquire without unreasonable effort or expense that is necessary to verify the accuracy of the information furnished to it, (iv) that they are aware that the securities concerning the Investment have not been registered under the Act, (v) that they are aware that their right to transfer, assign or otherwise dispose of their interest in the Investment is restricted by the Act and by applicable state securities laws, (vi) that they are aware there is no market for the securities and that no such market may ever develop and (vii) that they are persons of substantial financial means who have no need for liquidity in and are prepared to lost their entire investment in the Investment.

Subject to the provisions of their plan documents, the participation in Investments may be a suitable investment for (1) qualified pension, profit-sharing and other employee retirement benefit plans (including Keogh Plans), (ii) trusts and bank commingled trust funds for such plans and (iii) assuming the provisions of their governing instruments and the nature of their tax exemptions permit such an investment, other entities exempt from federal income taxation, such as individual retirement accounts, endowment funds and foundations and charitable, religious, scientific or educational organization, all of which are hereinafter referred to collectively as “Tax-Exempt Entities”. Fiduciaries of Tax-Exempt Entities, in consultation with their advisors, should carefully consider (i) whether participation is consistent with their fiduciary responsibilities, (ii) the effect of the possible treatment of such participation in investments and (iii) other tax risks.

The satisfaction of the suitability standards referred to above does not necessarily mean that the participation is a suitable investment for a prospective investor. LCM may make or cause to be made such further inquiry and obtain such additional information, as it deems appropriate with regard to the suitability of prospective investors. LCM, in its absolute discretion, may reject subscriptions, in whole or in part or allot to a particular investor less than the amount subscribed for. LCM reserves the right to modify or waive (other than for New York investors and other than with respect to “Accredited Investors” standards set forth in Regulation D) or increase the suitability standards with respect to certain investors, in order to comply with any applicable state or local laws, rules or regulations or otherwise.

We use cookies to improve your experience on our site. By using our site, you consent to cookies.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Google Tag Manager simplifies the management of marketing tags on your website without code changes.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Facebook Pixel is a web analytics service that tracks and reports website traffic.

Service URL: www.facebook.com (opens in a new window)

A video-sharing platform for users to upload, view, and share videos across various genres and topics.

Service URL: www.youtube.com (opens in a new window)

Levine Capital's Ground Up Construction Loans give real estate investors the leverage and flexibility to break ground faster. Competitive terms, investor-first underwriting, and capital structured around your 1-4 unit residential build.

Private capital built around how serious real estate investors actually operate.

Two purpose-built programs designed around your track record and project scope.

Bringing a modular build to market? We finance modular home projects nationwide under our Ground-Up Construction program.

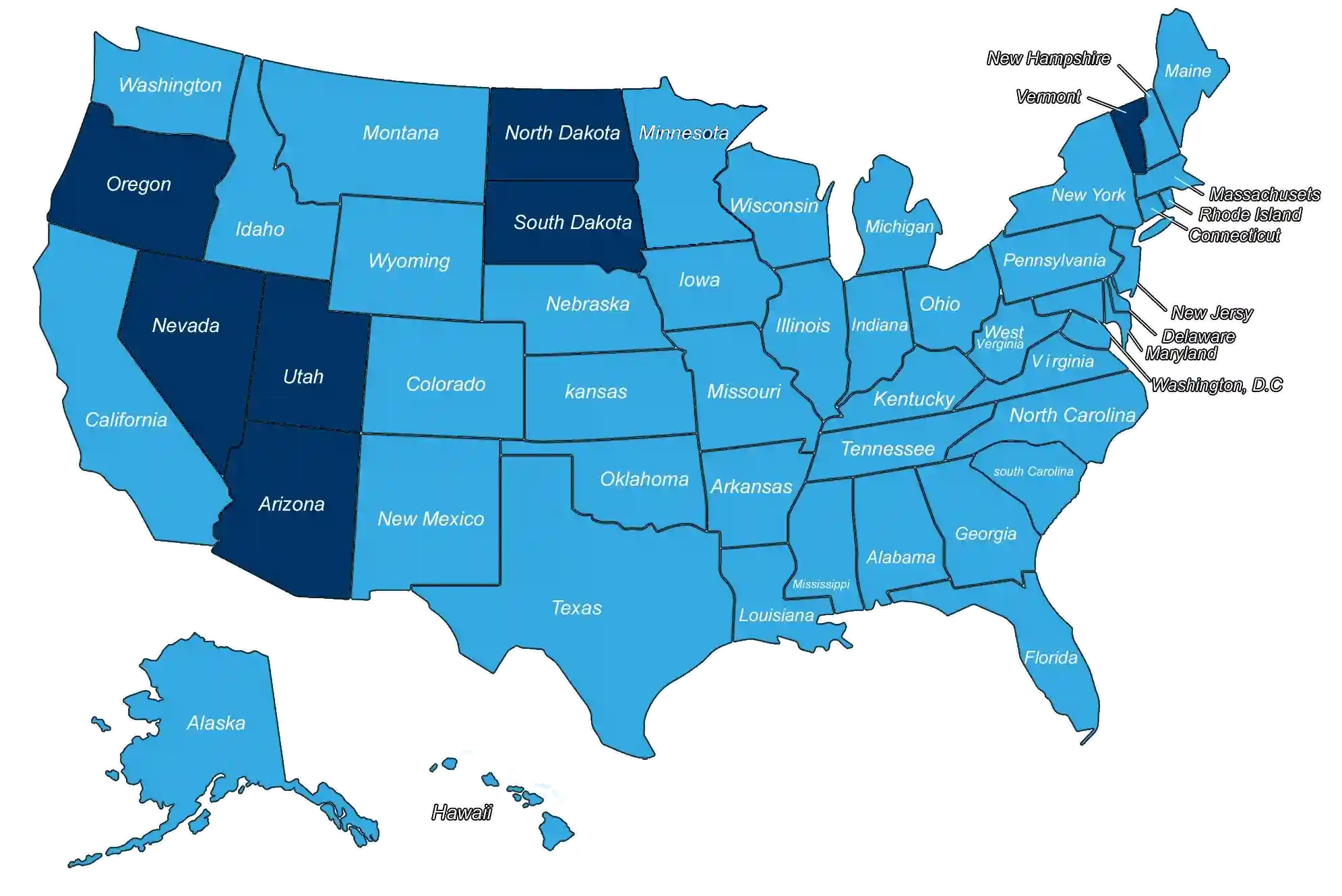

Nationwide coverage across our active lending markets.

Get a fast, no-obligation quote from a lender that closes when it counts.

* Non-owner-occupied loans only. All products are intended for residential investment properties.

** Rates shown reflect the lowest available pricing. Actual rates and terms are subject to approval criteria including FICO, experience, ownership duration, and other underwriting factors.

*** Levine Capital does not currently lend in: Arizona, Nevada, North Dakota, Oregon, South Dakota, Utah, and Vermont.