Debt Service Coverage Ratio (DSCR) loans are a go-to financing option for real estate investors looking to qualify based on rental income rather than personal income. Since these loans are often securitized and sold in the secondary market, lenders must follow strict underwriting guidelines to ensure the accuracy and reliability of property valuations.

Key requirement in the DSCR loan process is the use of two appraisals:

Key Components:

🔹Property Value: The appraiser determines the fair market value of the property based on recent comparable sales.

🔹Rental Income Assessment (1007 Form): Since DSCR loans rely on rental income, the appraisal includes a rent schedule (Form 1007), which estimates the market rent based on similar rental properties in the area.

🔹Condition & Marketability: The appraiser notes any deficiencies, repairs needed, or unique characteristics that may impact the property’s value.

This initial appraisal sets the foundation for the loan by establishing the property’s value and rental potential.

Key Components:

🔹Validation of the First Appraisal: The third-party reviewer cross-checks the original appraisal’s findings using automated valuation models (AVMs), recent market data, and comparable sales.

🔹Risk Assessment: The CDA/ARR flags inflated values, discrepancies, or unsupported adjustments that could make the loan riskier for securitization.

🔹Rental Income Confirmation: The rent schedule is analyzed independently to ensure the original appraiser’s rent estimates are in line with market conditions.

DSCR loans are often bundled into mortgage-backed securities (MBS) and sold to institutional investors. To reduce risk and maintain market confidence, investors require an extra layer of due diligence before purchasing these loans.

Without a CDA/ARR, lenders could inadvertently securitize loans based on overvalued properties or inaccurate rental projections, increasing the risk of losses in the secondary market.

Both appraisals are crucial for ensuring loan integrity, accurate underwriting, and market stability. Here’s how they work together:

| Step | Purpose |

|---|---|

| As-Is Appraisal with Rent Schedule | Establishes the market value and rent potential through a traditional appraisal. |

| CDA/ARR (Third-Party Review) | Validates the appraisal for securitization, ensuring it meets industry standards and investor requirements. |

By requiring these two appraisals, lenders protect both themselves and secondary market investors from unnecessary risk while ensuring DSCR loans remain a viable and scalable financing option.

If you’re seeking a DSCR loan, understanding the two-appraisal process is essential. The as-is appraisal verifies property value and rental income, while the CDA/ARR ensures securitization compliance by acting as a risk management tool.

At Levine Capital, we streamline the DSCR loan process with quick underwriting and competitive financing solutions. Whether you’re a seasoned investor or just starting, our Quick Quote allows you to submit your scenario in just five minutes and receive expert guidance on maximizing your financing options.

✔ Need Business Credit? Get expert guidance from Business Credit Workshop to build and scale your investment business.

✔ Interested in Creative Financing? Learn how to leverage Subto strategies with Subto to structure creative real estate deals.

Need funding for your next investment property? Get pre-qualified today and take advantage of our DSCR loan programs! 🚀

Subscribe to our YouTube channel to discover more about us.

We use cookies to improve your experience on our site. By using our site, you consent to cookies.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Google Tag Manager simplifies the management of marketing tags on your website without code changes.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Facebook Pixel is a web analytics service that tracks and reports website traffic.

Service URL: www.facebook.com (opens in a new window)

A video-sharing platform for users to upload, view, and share videos across various genres and topics.

Service URL: www.youtube.com (opens in a new window)

Levine Capital's Ground Up Construction Loans give real estate investors the leverage and flexibility to break ground faster. Competitive terms, investor-first underwriting, and capital structured around your 1-4 unit residential build.

Private capital built around how serious real estate investors actually operate.

Two purpose-built programs designed around your track record and project scope.

Bringing a modular build to market? We finance modular home projects nationwide under our Ground-Up Construction program.

Nationwide coverage across our active lending markets.

Get a fast, no-obligation quote from a lender that closes when it counts.

* Non-owner-occupied loans only. All products are intended for residential investment properties.

** Rates shown reflect the lowest available pricing. Actual rates and terms are subject to approval criteria including FICO, experience, ownership duration, and other underwriting factors.

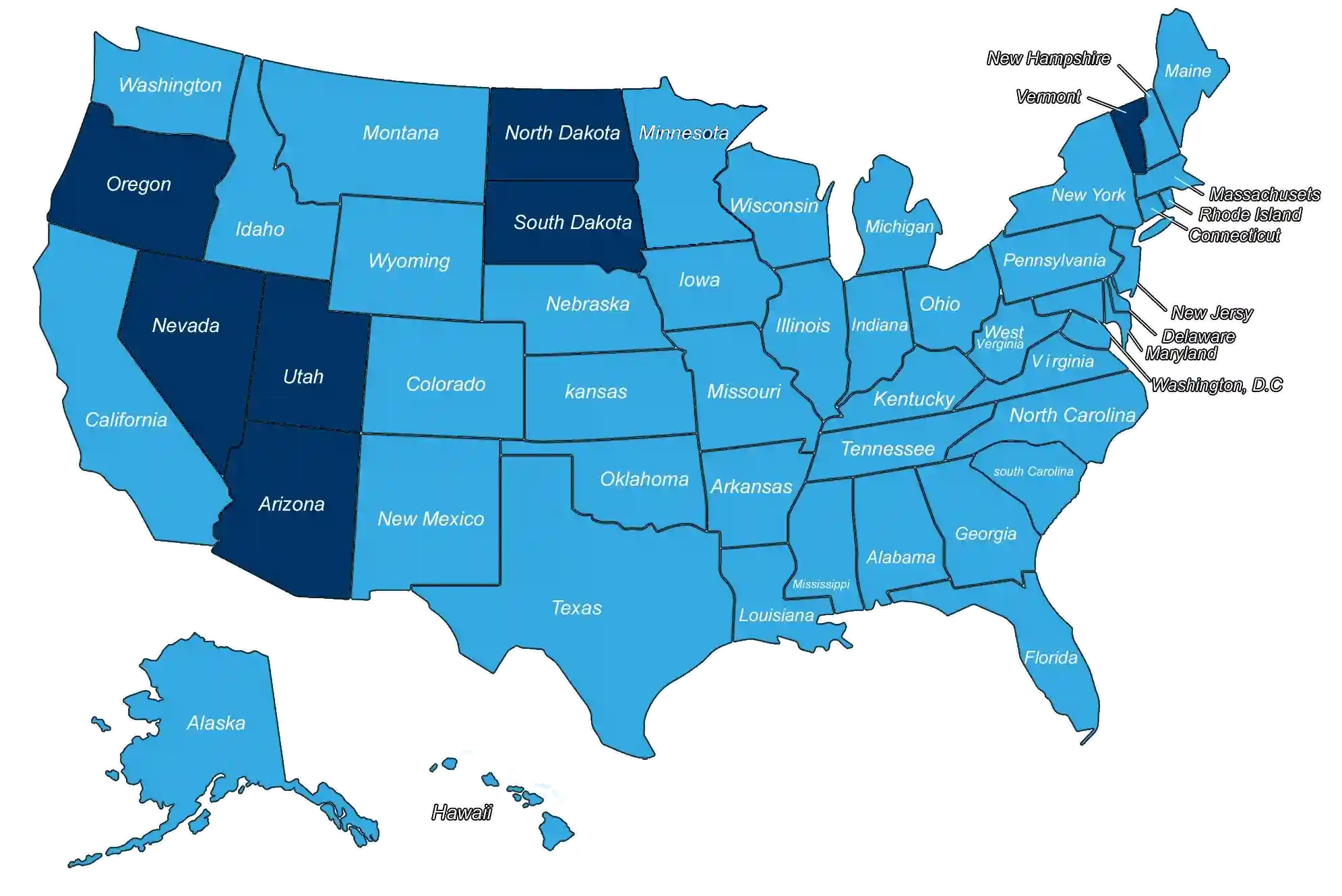

*** Levine Capital does not currently lend in: Arizona, Nevada, North Dakota, Oregon, South Dakota, Utah, and Vermont.